In stablecoin compliance, one issue is often underestimated: a sanctions hit is not the end of the process. It is the beginning of the case.

Many institutions start with sanctions lists, blacklisted addresses, KYT scores, and screening vendors. Those controls are necessary. But once stablecoins are used in payments, settlement, custody, OTC flows, or cross-border business, regulators and banking partners usually ask a more specific set of questions:

- What did the institution know before the transaction was executed?

- Why was the transaction allowed, escalated, blocked, frozen, or reported at that time?

- When risk information changed later, were historical transactions screened again?

- If an issuer freeze failed or funds had already moved, did the institution continue tracing the exposure?

- Is there an evidence trail that can be reviewed by audit, regulators, banking partners, and management?

This article looks at three recent and recurring problems in stablecoin sanctions compliance:

- Garantex: a sanctioned actor may continue to move through stablecoin networks after designation.

- A7A5 / Grinex: risk may sit in the structure around an asset, issuer, bank, exchange, and jurisdiction, not only in a single wallet address.

- USDT / USDC freezing research: contract-level freeze capability does not guarantee execution-level success.

The practical question for institutions is not whether they have purchased a third-party tool. Most institutions will use ChainTrust or a comparable provider as core infrastructure. The real question is how ChainTrust output becomes an operational process: screening, explanation, evidence, case handling, and continuous monitoring.

1. Garantex: Sanctions Do Not Automatically Stop Fund Flows

Garantex is a useful reference case because it shows why sanctions screening cannot stop at direct list matching.

The exchange was sanctioned by OFAC in April 2022 for its links to darknet markets, ransomware, and illicit finance. Public reporting and later law-enforcement actions showed that Garantex-related flows continued to matter in Russian-linked payment and stablecoin activity. In March 2025, U.S. authorities announced further enforcement action, including domain seizures and the freezing of approximately USD 26 million in crypto assets.

The key lesson for an institution is not simply "do not transact with Garantex." The more useful lesson is:

A sanctioned entity does not instantly lose its fund-flow network after being named.

Risk can migrate in at least three ways:

- Address migration: old wallets go inactive; new wallets inherit the same function.

- Channel migration: direct exposure declines while flows move through intermediaries, OTC desks, payment agents, or new exchanges.

- Entity migration: customers, merchants, technical infrastructure, and liquidity pools shift to related or successor platforms.

For Garantex-type risk, a yes/no screen is not enough. Institutions need to answer:

- Did the counterparty have direct exposure to known Garantex addresses?

- Did funds pass through downstream aggregation addresses associated with the same network?

- Is there evidence of old wallets being retired and new wallets taking over the same role?

- Are there stablecoin conversion, short relay, rapid splitting, or repeated small-value path patterns?

- When a new label or enforcement action appears, which historical customers and transactions are affected?

If these questions cannot be answered, it becomes difficult for an institution to prove that it did not help a high-risk network continue operating through new paths.

2. A7A5: Risk May Sit in the Structure, Not the Address

A7A5 illustrates a second problem: stablecoin sanctions risk may come from the financial structure around a transaction, not only from a direct wallet hit.

Public reporting has described A7A5 as a ruble-linked stablecoin used in Russian-linked cross-border payment scenarios. Reporting has also discussed alleged links among A7A5, Grinex, sanctioned banking infrastructure, and Russian shadow payment networks. Other public reports have raised questions around Kyrgyzstan-linked infrastructure and officials allegedly helping Russia evade sanctions.

Institutions should be careful here. Media investigations are not the same thing as legal determinations. A compliance decision should distinguish among:

- official sanctions or regulatory publications;

- media investigations;

- on-chain transaction facts;

- third-party labels;

- internal KYC / KYB data;

- customer explanations and counter-evidence.

Still, the A7A5 discussion is useful because it shows why single-address screening can miss structural risk.

The relevant question is not only:

Is this address on a sanctions list?

It is also:

Does this payment path help route value around a restricted financial system?

That requires looking at a broader graph:

- Who is the issuer?

- Which banks, reserve arrangements, custodians, or exchanges are connected?

- Which jurisdictions are involved?

- Who are the dominant user groups?

- Is the payment used for cross-border settlement involving sanctioned economies?

- Does the path connect to customers, successor infrastructure, or liquidity routes associated with a sanctioned exchange?

- Are restricted assets being converted into USDT, USDC, or other stablecoins through intermediate routes?

This is where a sanctions risk graph is more useful than a single address score. The graph links stablecoins, issuers, banks, exchanges, related entities, jurisdictions, address clusters, and fund-flow paths so that a compliance team can explain either side of a decision:

There was no direct SDN hit, but we escalated the transaction because it had indirect exposure to a high-risk network.

Or:

The transaction passed through a higher-risk geography, but the evidence did not support a sanctions escalation under our policy.

3. USDT / USDC Freezing: Freeze Is an Action, Not a Guarantee

Many institutions treat issuer-level freeze or blacklist capability as the final control. That is risky.

A 2026 research paper, Ordering Power is Sanctioning Power, argues that although centralized stablecoins can freeze addresses at the contract level, the freeze transaction itself still needs to be executed on-chain. If the sanctioned address submits a transfer and the issuer submits a freeze transaction around the same time, the final outcome may depend on block production, transaction ordering, and MEV dynamics rather than a regulatory instruction alone.

The study examines USDT and USDC sanctions enforcement data on Ethereum from November 2017 to August 2025 and reports cases where sanctioned addresses were emptied before a freeze became effective.

For institutions, the implication is straightforward:

- Pre-transaction screening cannot be skipped. An institution cannot wait for the issuer to freeze an address and then claim its own controls were sufficient.

- In-transaction controls must be owned by the institution. If internal policy identifies a high-risk payment, the institution needs the ability to pause, block, reject, or route it to review before settlement, withdrawal, or custody transfer.

- Post-transaction tracing must continue. Even if a freeze fails, the institution still needs to trace fund movement, downstream exposure, related customers, and historical transactions.

- The response record matters. Regulators do not only look at the outcome. They look at what the institution reasonably knew and did at the time.

In other words, freeze capability is not the compliance loop. The loop is:

Detect risk -> determine obligation -> execute action -> record evidence -> monitor for change.

4. Third-Party Services Are Not Outsourced Responsibility

Most institutions will not build address attribution, transaction graphing, sanctions monitoring, and evidence management from scratch. They will buy infrastructure from providers such as ChainTrust.

But buying a third-party service is not the same as outsourcing responsibility. The institution still owns customer onboarding, transaction disposition, freeze or rejection decisions, reporting, and audit records. ChainTrust's role is to turn on-chain facts into evidence that the institution can review, use, and retain.

In practice, this boundary has two layers:

- ChainTrust handles the on-chain layer: address attribution, fund-flow paths, risk labels, exposure distance, rule hits, data sources, and historical re-screening.

- The institution handles the business layer: customer identity, transaction purpose, contracts, invoices, applicable law, risk appetite, approval decisions, and final disposition.

Once a stablecoin transaction enters a compliance workflow, the useful question is not "what score did the tool return?" It is:

What evidence was recorded before, during, and after the transaction?

Layer 1: Pre-Transaction Risk Packet

Before a transaction executes, the goal is not to "check whether an address has a problem." The goal is to give the institution a usable judgment packet.

ChainTrust should return explainable fields that can be stored in an approval record:

- address ownership or attribution;

- related entities and clusters;

- direct and indirect exposure;

- exposure distance;

- key labels and data sources;

- suspicious behavior such as rapid relay, splitting, aggregation, or circular transfer;

- recommended action;

- case link and graph snapshot.

For structural risks such as A7A5, the system should not only look at the address. It should place issuers, exchanges, banks, jurisdictions, conversion paths, and related entities into the same risk graph.

The institution then adds off-chain context: KYC / KYB, beneficial ownership, business type, transaction purpose, invoices, contracts, customer history, and internal policy. The resulting record is the Pre-Transaction Risk Packet.

Layer 2: Response Evidence Pack

During transaction handling, the worst design is a vague "high risk" pop-up that leaves the business team to decide what to do.

In CT Probe, a rule hit should become a case. The case should contain:

- transaction hash or proposed transaction;

- address, chain, asset, amount, and time;

- fund-flow path;

- risk labels and triggered rules;

- data source and rule version;

- graph snapshot;

- reviewer notes and final disposition.

The institution adds customer explanations, contracts, invoices, payment instructions, legal analysis, approval comments, and final actions. This combination becomes the Response Evidence Pack.

If a regulator later asks why a transaction was not blocked, a weak answer is:

The system score was not high.

A reviewable answer is closer to:

At the time, ChainTrust identified no direct sanctions hit but flagged two-hop exposure to a high-risk network. We paused the transaction, requested supporting documents, reviewed the customer explanation, approved a limited release under internal policy, and scheduled a 30-day review.

That is the difference between a score and an evidence system.

Layer 3: Continuous Monitoring

Stablecoin sanctions risk changes quickly. Address attribution, entity relationships, media investigations, law-enforcement actions, and official sanctions lists all evolve.

Continuous monitoring should re-screen historical exposure when:

- a sanctions list is updated;

- new Garantex, Grinex, A7A5, or related labels appear;

- law enforcement publishes new wallets or entities;

- issuer freeze lists change;

- a historical downstream path becomes high risk.

A useful monitoring alert does not simply say "risk increased." It should answer:

- What event triggered the alert?

- Which customers, addresses, transactions, and cases are affected?

- What is the exposure distance?

- What amount is affected?

- What evidence changed?

- What action does ChainTrust recommend?

- Does the institution need to reopen approval, file a report, restrict activity, or update internal rules?

The objective is not to predict the future. It is to prove that when risk information changed, the institution could identify affected historical activity and complete a timely review.

5. A CT Probe Case: The Point Is Not a Score

The easiest misunderstanding is to treat CT Probe as a tool for checking an address score.

Real investigations work differently. When a compliance analyst opens a case, the first questions are:

- Where did this risk lead come from?

- Which nodes did the funds pass through?

- Is the evidence strong enough to support the next action?

Step 1: Put the Address Back Into the Path

In Garantex, A7A5, and similar scenarios, a single address often has limited meaning. The relationship between addresses matters more.

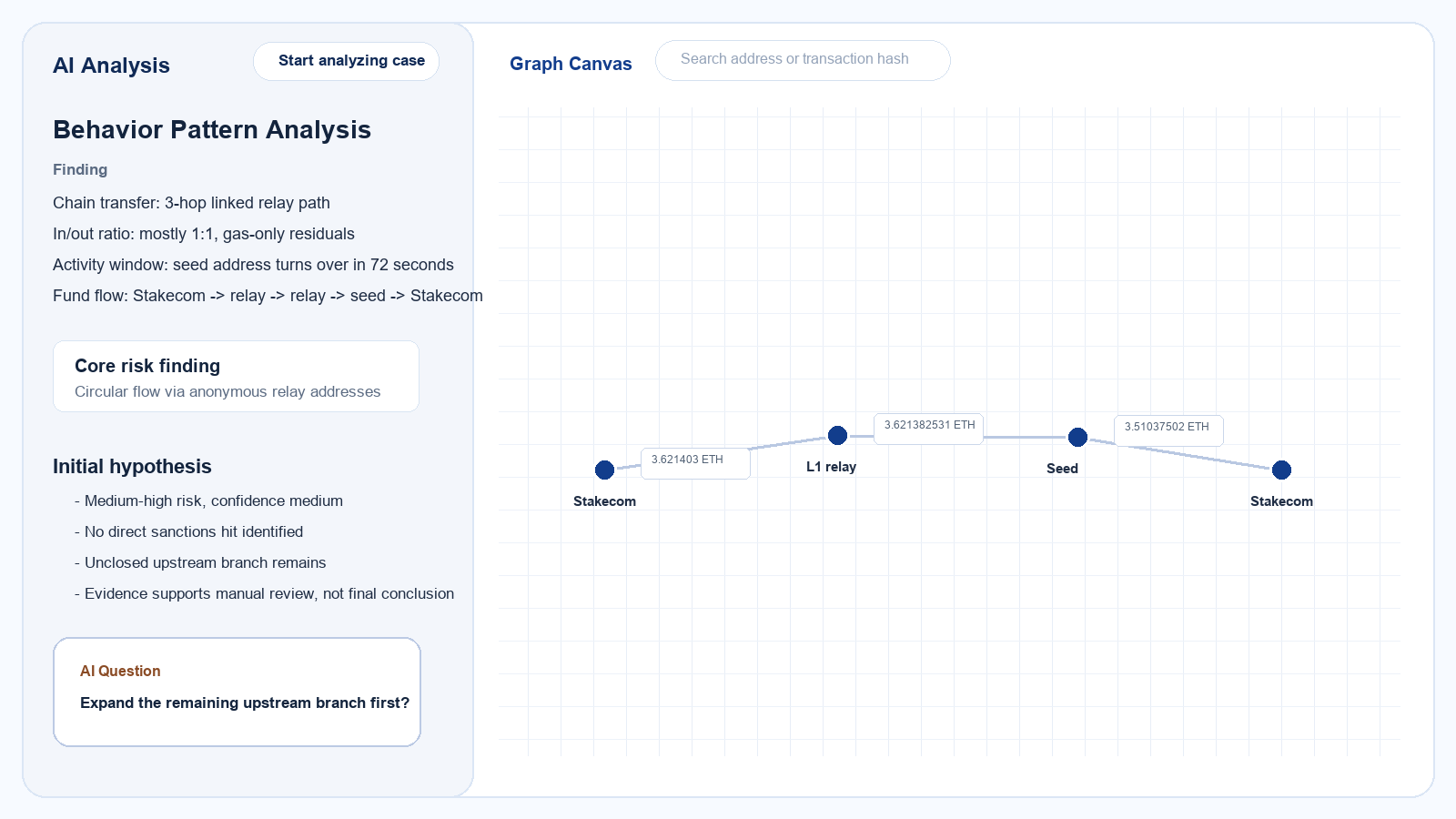

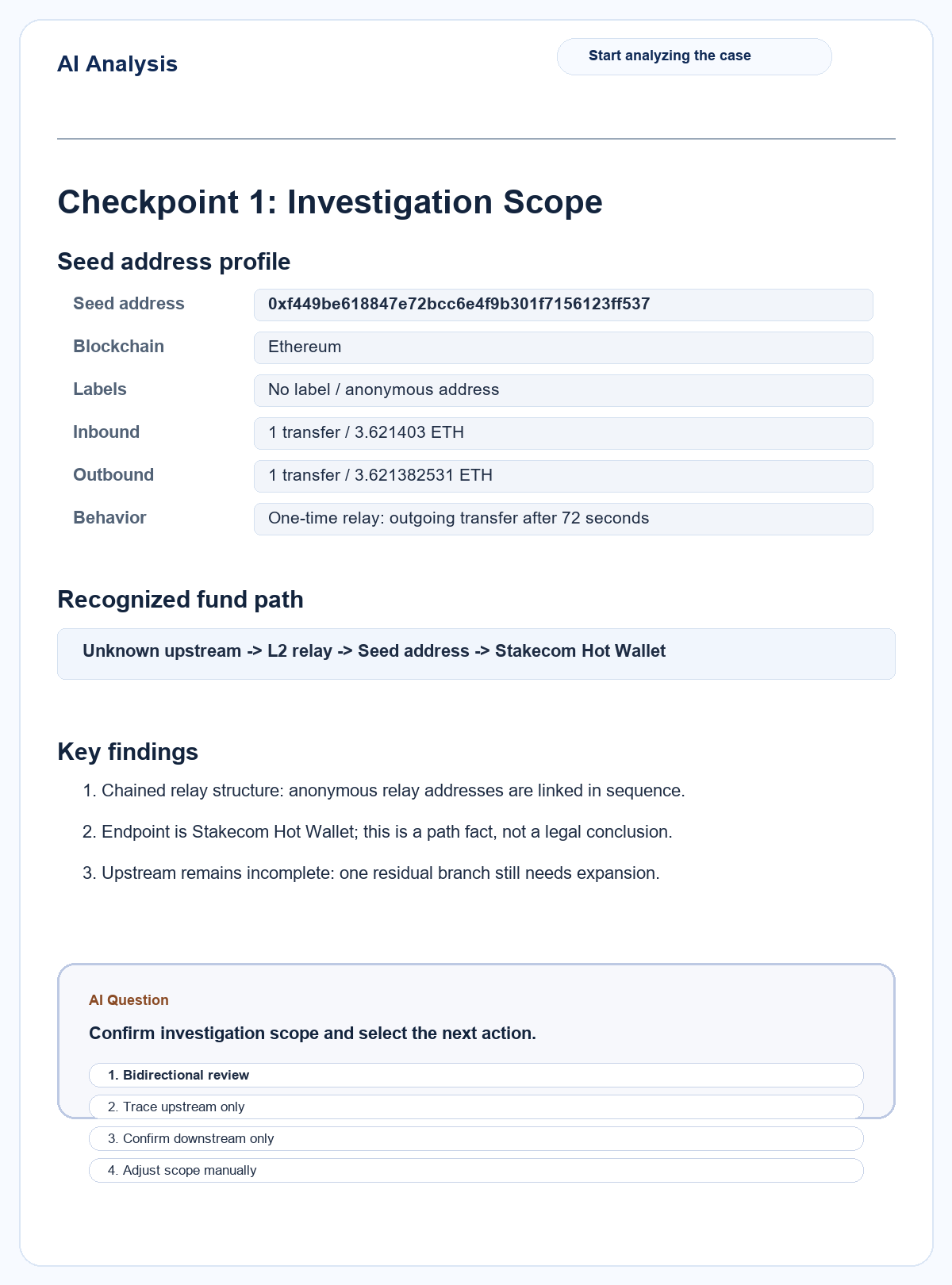

In this CT Probe example, the seed address is:

0xf449be618847e72bcc6e4f9b301f7156123ff537

Viewed alone, the address has only one inbound transfer and one outbound transfer. It receives 3.621403 ETH and sends out 3.621382531 ETH. The residual is essentially gas. It has no label and no complex interaction pattern.

After upstream tracing, CT Probe identifies a more complete path:

| Layer | Address | CT Probe identification | Key fact |

|---|---|---|---|

| L0 | 0x974caa59e49682cda0ad2bbe82983419a2ecc400 | Stakecom Hot Wallet | Two ETH transfers to L1 on 2025-02-21: 3.51037502 and 3.55704206 ETH |

| L1 | 0xe09173b168cbecefc0964c3adcf24e19e01927b2 | Unlabeled relay address | 2 in / 2 out, around 7.067 ETH; 3.621525 ETH moves to L2; another roughly 3.45 ETH branch remains to be traced |

| L2 | 0x72a3cc02ba2b8a4bcbe0b01d900a70bc5d839fa5 | Unlabeled relay address | 1 in / 1 out, sends 3.621403 ETH to the seed address |

| L3 | 0xf449be618847e72bcc6e4f9b301f7156123ff537 | Seed address | 1 in / 1 out, sends 3.621382531 ETH back to Stakecom Hot Wallet after 72 seconds |

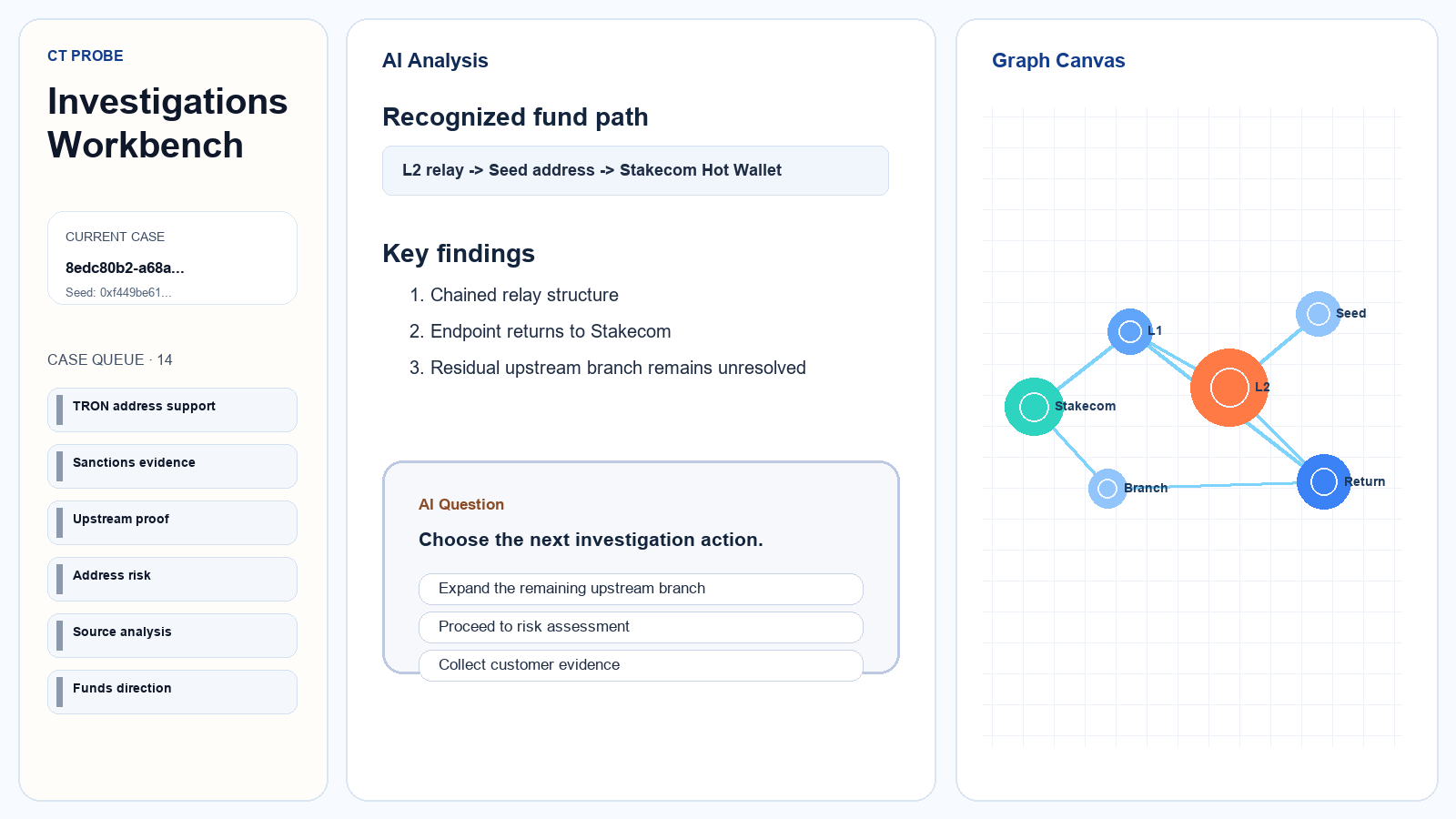

The path is not simply "unknown address -> target address -> platform." It is:

Stakecom Hot Wallet -> anonymous relay L1 -> anonymous relay L2 -> seed address -> Stakecom Hot Wallet

This case does not label Stakecom as a sanctions risk and does not equate a gaming or betting platform label with an illegal conclusion. It demonstrates a more basic institutional problem:

Some risks are not written into address labels. They appear in fund-flow relationships.

CT Probe separates the evidence:

- the target and upstream addresses are anonymous relay addresses with narrow behavior;

- each layer leaves almost only gas residuals;

- the path forms a circular return: Stakecom out, multiple anonymous relays, Stakecom back;

- one residual branch from L1 remains untraced;

- the system records a medium-high risk hypothesis and asks whether the remaining branch should be expanded.

For a compliance analyst, the question is not "does this address have a red label?" The question is:

Why does an unlabeled address route funds from the same platform through anonymous relays and then back to the same platform? Does the untraced branch show a similar pattern? Is this enough to trigger manual review or customer explanation?

Step 2: Separate Facts, Labels, and Inferences

Many risk mistakes come from mixing materials with different evidentiary weight.

Official sanctions documents, on-chain transaction facts, third-party labels, media investigations, customer explanations, and internal approval notes can all belong in a case. But they should not be treated as the same type of evidence.

In CT Probe, the evidence can be separated into:

- Upstream crime: whether funds originate from known crime, enforcement, or sanctions-linked sources;

- Fund flow: path, exposure distance, amount, and timing;

- Behavioral anomaly: rapid relay, splitting, aggregation, circular transfer;

- Subjective knowledge: customer explanation, contracts, invoices, chat records, internal approval, and other off-chain materials.

This helps the compliance team distinguish:

- what is an on-chain fact;

- what is third-party attribution;

- what is only a lead;

- what has been reviewed;

- what still needs customer documentation.

In this case, CT Probe does not write a final conclusion such as "illicit funds" or "sanctions hit." It first records verifiable facts: one inbound and one outbound transfer, an upstream anonymous relay, and a downstream Stakecom Hot Wallet. It then separates findings such as relay behavior, platform endpoint, and incomplete upstream source.

That is closer to how institutions need to answer internal review and external questions: known facts, inferences, and missing evidence are kept separate.

Step 3: Turn the Case Summary Into the Next Action

The graph and evidence list answer "what happened." A case summary should answer "what should happen next."

A useful CT Probe case summary should provide:

- risk level;

- triggered rule;

- key evidence;

- affected amount;

- related addresses and transactions;

- recommended action;

- review status;

- monitoring requirement.

The recommended action cannot stop at "high risk." It should be operational:

- allow: release and retain the record;

- review: pause and route to manual review;

- request documents: ask the customer for supporting material;

- block: reject or freeze, subject to applicable law;

- monitor: release but continue monitoring.

The final decision remains with the institution. ChainTrust provides evidence, paths, and recommended actions. The institution applies its legal obligations, customer file, and risk policy.

6. How Institutions Operationalize ChainTrust

If an institution has already purchased ChainTrust, implementation is not about rebuilding on-chain analytics. It is about embedding ChainTrust output into customer, transaction, approval, and reporting workflows.

Step 1: Bring monitored objects into ChainTrust

The first step is to onboard the objects the institution actually cares about:

- proprietary wallets;

- customer deposit addresses;

- customer withdrawal addresses;

- custody addresses;

- hot and cold wallets;

- operating wallets;

- high-frequency counterparties;

- approved counterparties;

- rejected or frozen addresses;

- historical high-risk cases.

ChainTrust builds a monitoring profile around these objects: attribution, fund flows, labels, exposure, related cases, and current risk state.

Step 2: Map ChainTrust outputs to internal policy

ChainTrust can identify risk evidence. The institution decides how that evidence maps to policy.

For example:

| ChainTrust signal | Typical institution decision |

|---|---|

| Direct sanctions hit | reject, freeze, escalate, or report under applicable law |

| One-hop exposure to a sanctioned or prohibited service | pause and compliance review |

| Multi-hop exposure to a high-risk network | enhanced due diligence |

| Circular relay or rapid pass-through behavior | request explanation or documents |

| Low risk with no adverse path | allow and retain evidence |

The institution should document the mapping so decisions are consistent across teams and time.

Step 3: Create cases automatically

When a transaction triggers review, the event should not remain as a chat note or generic ticket.

The system should create or update a CT Probe case containing:

- case ID;

- trigger rule;

- address, chain, asset, amount, and time;

- transaction hash or proposed transaction;

- fund-flow graph;

- evidence list;

- recommendation;

- reviewer notes;

- final action;

- monitoring follow-up.

This is where ChainTrust becomes more than screening infrastructure. It becomes the evidence layer behind institutional decisions.

Step 4: Re-screen historical exposure

When labels, enforcement actions, or issuer freeze lists change, ChainTrust should identify which historical customers, addresses, cases, transactions, and amounts are affected.

The institution then decides whether to:

- reopen a case;

- re-rate a customer;

- restrict future activity;

- request additional documents;

- file SAR / STR or equivalent reports;

- notify internal management, banking partners, or custodians;

- update internal policy.

Step 5: Export audit-ready material

For management, legal, audit, or regulatory review, a useful package should include:

- Executive Summary What happened, how large the exposure was, and what action was taken.

- Investigation Report Fund path, evidence source, triggered rule, reviewer reasoning, and disposition.

- Transaction Appendix Hashes, addresses, timestamps, assets, amounts, exposure distance, and case references.

The institution's final record should combine ChainTrust evidence with internal approval and disposition. That is what makes the decision reviewable.

Conclusion: Stablecoin Compliance Is Moving From Screening to Evidence

Garantex shows that sanctioned actors can continue seeking stablecoin routes after designation.

A7A5 shows that risk can sit in the structure around an asset, issuer, bank, exchange, and jurisdiction.

USDT / USDC freezing research shows that freeze capability is necessary but not sufficient as an execution guarantee.

For institutions, the useful third-party compliance infrastructure must answer four questions:

- How does ChainTrust identify and explain risk before a transaction?

- How does ChainTrust turn a rule hit into an actionable case during transaction handling?

- How does ChainTrust re-screen historical exposure after risk information changes?

- How does the institution combine ChainTrust evidence with internal approval, disposition, and reporting?

This is where ChainTrust and CT Probe are most relevant:

- Risk Graph explains the network, not only the address.

- Response Evidence Pack preserves the reasoning behind the action.

- Continuous Monitoring re-screens historical customers and transactions as risk changes.

Stablecoin compliance is no longer only about whether a name or address was screened.

The real question is:

When a list hit, label update, freeze failure, or fund migration occurs, can ChainTrust help the institution produce evidence, and can the institution make an auditable decision based on that evidence?

References

- U.S. Treasury, "Treasury Sanctions Russia-Based Hydra and Virtual Currency Exchange Garantex", 2022-04-05. https://home.treasury.gov/news/press-releases/jy0701

- U.S. Department of Justice, "Russian Cryptocurrency Exchange Garantex Taken Down", 2025-03-07. https://www.justice.gov/opa/pr/russian-cryptocurrency-exchange-garantex-taken-down

- Financial Times, "Crypto coin for Russian shadow payments moves $9bn", 2025-06-25. https://www.ft.com/content/1c71cac0-b86b-4361-8f54-ee5d3bb5a489

- The Guardian, "Take action over officials in Kyrgyzstan 'helping Russia evade sanctions', MPs and peers say", 2026-04-23. https://www.theguardian.com/world/2026/apr/23/take-action-over-officials-in-kyrgyzstan-helping-russia-evade-sanctions-mps-and-peers-say

- Di Wu et al., "Ordering Power is Sanctioning Power: Sanction Evasion-MEV and the Limits of On-Chain Enforcement", 2026. https://arxiv.org/abs/2603.27739