Stablecoin discussions have often centered on two questions: whether reserves are real, and whether redemption is reliable. As regulatory frameworks continue to take shape, both questions remain important. But they are no longer the whole story.

As stablecoins move from exchange settlement assets into payments, cross-border transfers, DeFi, RWA, institutional treasury operations, and merchant acceptance, the core compliance challenge begins to change. Risk does not only arise at issuance. It also does not only arise at the moment a single transaction is submitted for screening. The harder problem is that once a stablecoin enters an open on-chain network, it continues to circulate across chains, entities, use cases, and time windows.

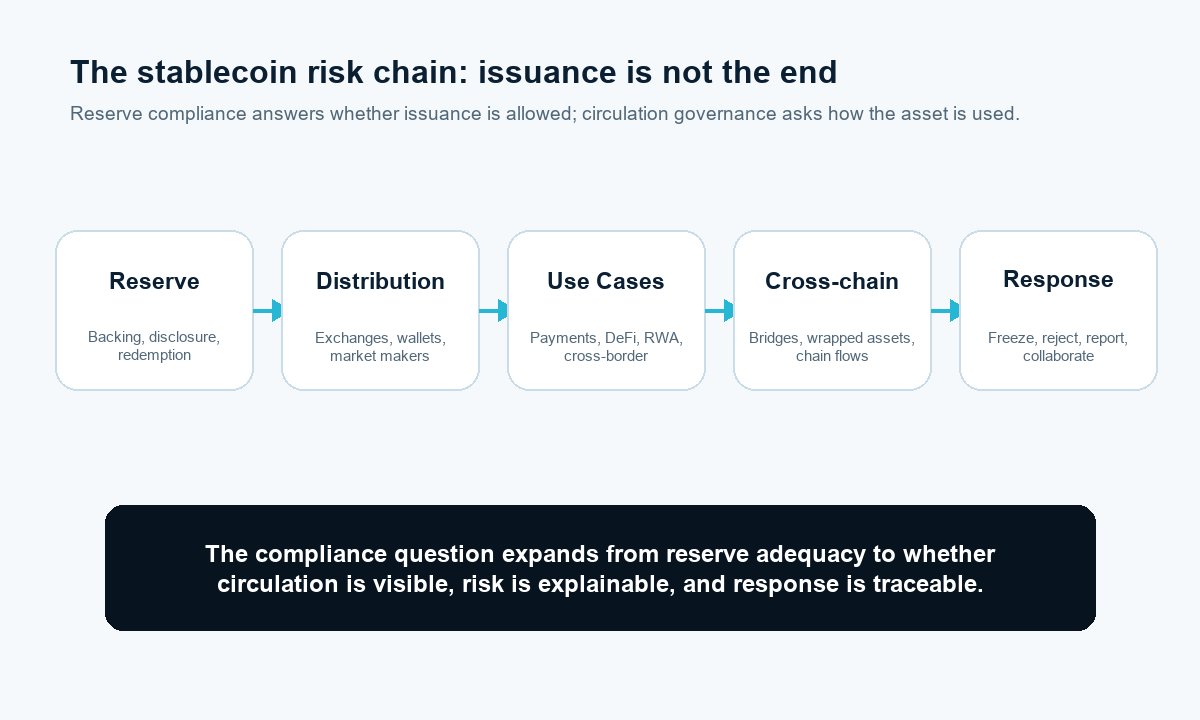

The next stage of stablecoin compliance is therefore not only issuance compliance. It is circulation risk governance.

Circulation risk governance is not an abstract concept. It refers to the ongoing management of on-chain usage, holding concentration, cross-chain migration, risk exposure, and response outcomes after a stablecoin has been issued. It asks not only whether a stablecoin can be issued, but how it is used in open networks and whether its risk remains continuously visible.

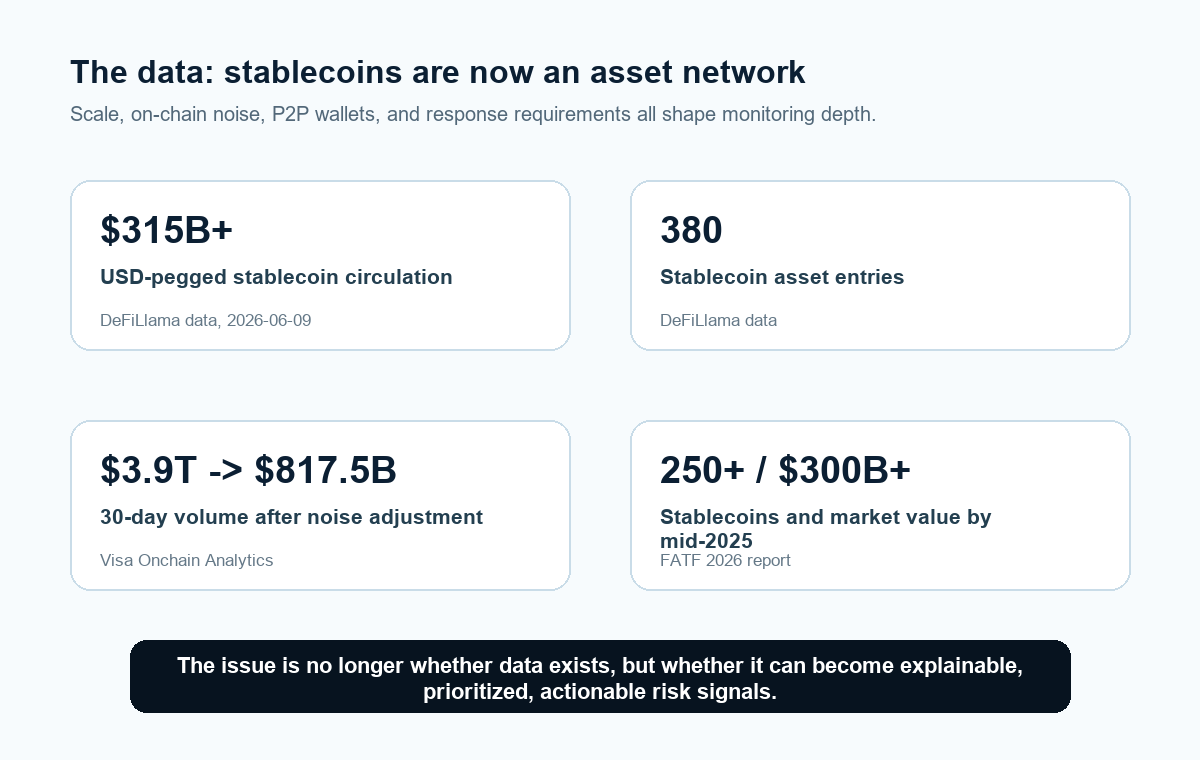

The data shows why this issue is becoming concrete. According to DeFiLlama stablecoin data on June 9, 2026, USD-pegged stablecoin circulation was approximately $315.25 billion, with about 380 stablecoin asset entries. USDT accounted for approximately $186.79 billion, while USDC accounted for approximately $76.05 billion. FATF's 2026 targeted report on stablecoins and unhosted wallets also noted that, by mid-2025, there were more than 250 stablecoins with a total market value above $300 billion.

Beyond scale, the risk lies in the complexity of what the data means. Visa's stablecoin analysis shows that 30-day raw stablecoin transaction volume can fall from $3.9 trillion to $817.5 billion after a simple heuristic adjustment. This does not mean raw data is useless. It means stablecoin activity contains substantial noise from bots, arbitrage, market making, smart contract interactions, and internal treasury movements. Compliance teams do not simply need more raw numbers. They need a metric system that can distinguish normal circulation, business activity, risk migration, and abnormal response scenarios.

1. Reserve Transparency Does Not Remove Circulation Risk

The first layer of stablecoin trust comes from reserves. For fiat-backed stablecoins, reserve assets, redemption mechanisms, audit disclosures, and regulatory qualifications are foundational to market confidence.

But reserve transparency does not mean that on-chain circulation is risk-free.

A stablecoin with compliant reserves can still be used for scam fund transfers, sanctions evasion, ransomware payments, illicit marketplace settlement, cross-chain money laundering, complex DeFi path splitting, or transfers involving P2P and unhosted wallets. FATF's 2026 report notes that stablecoins' price stability, high liquidity, and interoperability support legitimate uses, but also make them attractive for criminal abuse. The same report noted that by mid-2025, there were more than 250 stablecoins with a total market value above $300 billion.

This points to a practical reality: the closer stablecoins move toward payment and settlement infrastructure, the more they need to remain observable after issuance.

Issuers can prove reserves. VASPs can complete customer onboarding. Payment institutions can review merchants. But these actions only cover part of the risk within each participant's own boundary. Risk often emerges between boundaries: from custodial platforms to unhosted wallets, from CEXs to DEXs, from one chain to another, from ordinary transfers to bridges, and from merchant acceptance to secondary market circulation.

2. Stablecoin Data Is Visible, But Meaning Is Often Unclear

Stablecoin data is public on-chain. But public does not mean understandable.

Visa's stablecoin analysis highlights that stablecoin transaction data contains substantial noise. A transaction may represent a real payment, or it may come from bots, arbitrage, market making, contract interactions, internal rebalancing, or DeFi automation. Raw transaction volume can look large without necessarily representing real economic activity. Likewise, an ordinary-looking transfer may only be one step in a more complex path.

This raises the bar for compliance teams. Stablecoin monitoring cannot stop at whether transaction volume is increasing. It also cannot stop at whether an address already has a label. The data has to be translated into operational risk meaning:

- Which transactions look like real payments, and which look like automation or internal movement?

- Which addresses are technical nodes, and which represent real risk entities?

- Which balance concentrations come from normal market making, and which may create risk exposure?

- Which cross-chain flows are ordinary asset allocation, and which may indicate risk migration?

- Which alerts require immediate action, and which are low-priority noise?

The challenge is not that stablecoin data is unavailable. The challenge is that the data must be translated into an actionable risk language.

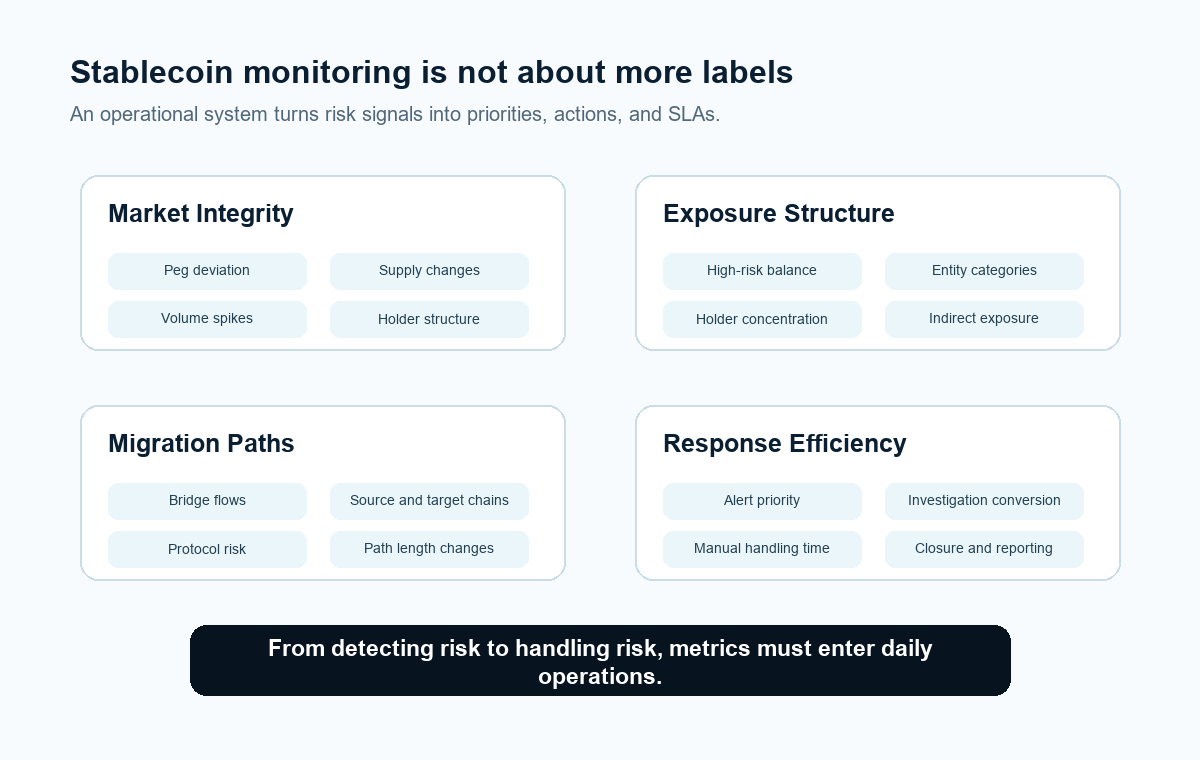

3. Circulation Risk Governance Needs Four Operational Metrics

If a stablecoin is treated as a continuously running asset network, monitoring cannot focus only on adding more labels. A more useful approach is to turn risk signals into operational metrics that teams can review, prioritize, investigate, and act on every day.

Market Integrity: Is the Stablecoin Still Operating Normally?

Market integrity focuses on whether the stablecoin is functioning as an asset: whether the price is deviating from its peg, whether supply changes are abnormal, whether transaction volume suddenly increases, whether holder counts behave unusually, and whether major holders are migrating.

For issuers and institutional users, these are not just market indicators. They are early risk signals. If the peg deviates, liquidity contracts, major holders move suddenly, or supply and usage patterns on a chain become abnormal, compliance and operations teams need to understand the cause quickly.

Exposure Structure: Where Are Risk Balances Accumulating?

Stablecoin risk is not only visible in individual transactions. It is also visible in balance structure.

If the share of balances held by high-risk entities rises, or if a certain type of risk entity begins receiving a stablecoin more frequently, risk may have shifted from isolated events into asset exposure. For VASPs, this affects deposit and withdrawal policy. For issuers, it affects secondary-market reputation risk. For payment institutions, it affects merchant and scenario management.

Exposure structure answers a practical question: are risk funds accumulating around certain entities, address clusters, or business scenarios?

Migration Paths: How Does Risk Move Across Chains?

The risk of a multi-chain stablecoin does not remain on one chain.

Bridges, wrapped assets, DEXs, liquidity pools, and intermediate wallets can all change the visibility of fund paths. A risk entity may not directly enter a regulated platform. It may first move through bridges, protocols, and newly created addresses before appearing at what looks like a clean entry point.

Stablecoin monitoring therefore needs to observe source chains, destination chains, bridge protocols, path length, changes in entity categories before and after bridging, and whether funds enter new high-risk scenarios after crossing chains.

Response Efficiency: Can the Team Act After Detection?

The final mile of stablecoin compliance is response.

If alerts cannot be prioritized, investigations cannot drill down, related addresses cannot remain under observation, and outcomes cannot be written back into the system, monitoring stops at seeing anomalies. A mature monitoring system should record alert priority, manual handling time, investigation conversion, closure reason, whether a report was filed, and whether freezing or redemption rejection was triggered.

This is the difference between circulation risk governance and a standard data dashboard. The former enters risk operations. The latter only displays data.

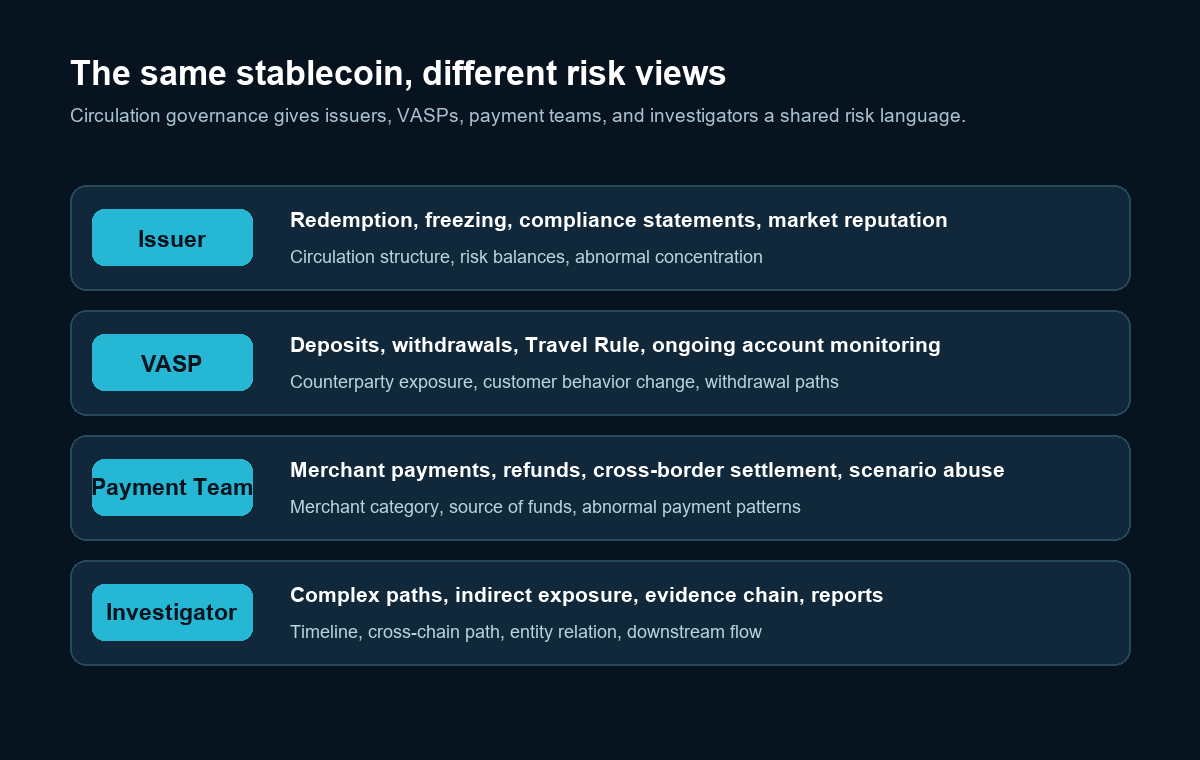

4. Different Participants Need a Shared Risk Language

Participants in the stablecoin network have different responsibilities.

Issuers focus on reserves, redemption, freezing, compliance statements, and secondary-market reputation. VASPs focus on customer onboarding, deposits, withdrawals, Travel Rule requirements, ongoing account monitoring, and suspicious activity reporting. Payment institutions focus on merchant acceptance, refunds, cross-border settlement, and scenario abuse. Investigation teams focus on complex paths, indirect exposure, entity relationships, and evidence chains.

Each role sees a different entry point into risk. Without a shared language, risk can easily be underestimated at the boundaries.

For example, when stablecoins move from an unhosted wallet into a merchant payment scenario, a payment institution may view it as a transaction risk issue. If the funds later enter a VASP withdrawal path, a trading platform may view it as a customer behavior issue. If the same funds have indirect exposure to sanctions, scams, or ransomware paths, issuers and investigators may need to consider freezing, collaboration, and reporting.

The same funds may be treated as different events in different systems. The purpose of circulation risk governance is to put those events back into the same asset network.

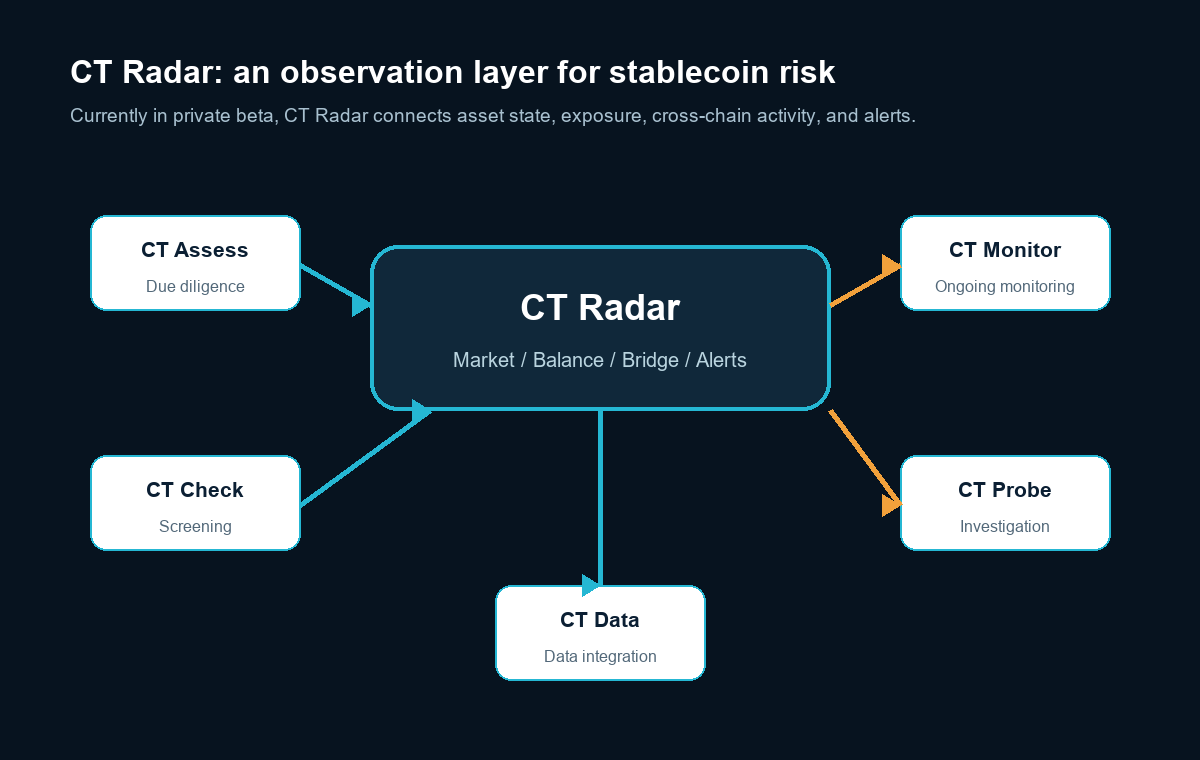

5. CT Radar: Turning Stablecoins Into Observable Risk Objects

Based on this view, ChainTrust is building CT Radar.

CT Radar is currently in private beta. It is not a product announcement or a simple market data page. It is a risk observation layer built around stablecoin circulation risk governance. From the Token + Chain level, it connects market state, holding structure, balance risk distribution, cross-chain activity, and real-time alerts.

It is designed to answer four practical questions:

- Is this stablecoin operating normally on the current chain?

- Which entity categories and specific entities concentrate risk balances?

- Is risk migrating through cross-chain paths?

- After an anomaly is detected, can the case move into CT Monitor and CT Probe for ongoing monitoring and investigation?

Within the ChainTrust product system, CT Assess supports partner, VASP, merchant, OTC, and institutional onboarding due diligence. CT Check supports address and transaction screening. CT Monitor supports ongoing transaction monitoring. CT Probe supports complex tracing, investigation, and report generation. CT Data provides labels, entities, risk scores, and behavioral signals for integration into business systems.

CT Radar brings these capabilities forward to the stablecoin asset layer. It first makes the circulation state of a token on a specific chain visible, then helps determine which addresses, transactions, entities, and paths should move into downstream handling.

6. The Next Step in Stablecoin Compliance Is Operational Risk Infrastructure

Stablecoins are moving from crypto trading venues into broader payment and settlement scenarios. Regulatory frameworks will continue to improve. Issuer disclosures will continue to strengthen. VASP transaction monitoring will also become more mature. But long-term trust depends on whether stablecoin circulation in open networks can be continuously understood and effectively governed.

For compliance teams, this means three things.

First, do not look only at static labels. Look at behavior, paths, and changes over time.

Second, do not look only at data inside a single platform. Look at stablecoin exposure across the on-chain network.

Third, do not only generate alerts. Turn alerts into prioritization, investigation, response, and feedback loops.

CT Radar is currently in private beta. If you are working on issuer risk dashboards, VASP ongoing transaction monitoring, payment-scenario risk detection, cross-chain fund observation, or stablecoin circulation risk governance, contact the ChainTrust team to learn more.

References

- FATF, Targeted Report on Stablecoins and Unhosted Wallets - Peer-to-Peer Transactions, 2026-03-03.

- FATF, Virtual Assets Red Flag Indicators of Money Laundering and Terrorist Financing, 2020-09-14.

- DeFiLlama, Stablecoins data, 2026-06-09.

- Financial Stability Board, High-level Recommendations for the Regulation, Supervision and Oversight of Global Stablecoin Arrangements, 2023-07-17.

- Visa, Making sense of stablecoins, 2025-07-21.

- The White House, The President Signed into Law S. 1582, 2025-07-18.

ChainTrust Labs

Learn more about ChainTrust KYT, on-chain risk monitoring, and investigation products: https://chaintrustlabs.com/